Full disclosure: When I first drafted an editorial calendar for this blog way back in January, I planned topics that would be contextually relevant and helpful for the time of year. My original intent for July, when all of us on this side of the pond celebrate the fourth, was to write about independence. Specifically, Financial Independence. (Pretty clever, eh?)

But with the amplifying voices and talk about a coming recession, I decided to switch gears a bit. I am by no means an expert on the topic, but I’ve lived through a few in my soon to be 61 years. And so, I offer you the benefit of financial lessons this writer’s learned the hard way. This is by no means financial advice. Just sharing a few tips and insights I’ve picked up over the years.

You can only control what you can control

“So, what kind of junior-Jedi, Yoda-esque crap advice is that?!” you may be asking. It’s really quite simple. You can’t control the economy. You can’t control inflation. You can’t control the stock market. But you can control you. Your reactions to all these factors — emotionally and financially.

Sure, the financial outlook may appear bleak. But don’t allow your emotions to run amok and drive you to make impulsive or irrational financial decisions. In fact, if you Googled “How to survive a recession,” I’ll bet that is one of the top 10 pieces of advice/tips. I would add to that, stop checking in on your 401(k)’s or IRA’s performance. It’s only going to be depressing. (I know this to be true firsthand.) So what can you do?

Stay committed to your future

While I strongly suggest you stop looking at your retirement account values, that is no way implying you stop contributing (as I mistakenly did in the past). In fact, I’d say be sure to stay the course, full steam ahead. When stocks values are down as they’ve been, their prices are lower. So you’re actually getting more shares (at a lower price) with your regular, automatic contributions. And when the economy improves (as it always does), the value of those stocks will rise too — and the overall value of your portfolio with it!

Some people use an event like this to “rebalance” their overall portfolio. Shifting even more of their money into stocks to take advantage of future potential gains when stock prices rebound. As with all important financial investment decisions, it’s best to seek professional advice, preferably an advisor who is a “fiduciary” (someone who is committed and required to act in your best interests).

If you find you absolutely need to reduce your retirement contributions temporarily, do try to maintain whatever’s required to earn the maximum of your company’s matching contribution. But before you make any changes, please read the next section.

Check in on your budget

The fact that you’re reading this blog speaks volumes about the type of thoughtful, financially-responsible person you are. So I feel quite safe in assuming that you not only set a budget, but actually stick to it. Maybe it’s time for a bit of tweaking.

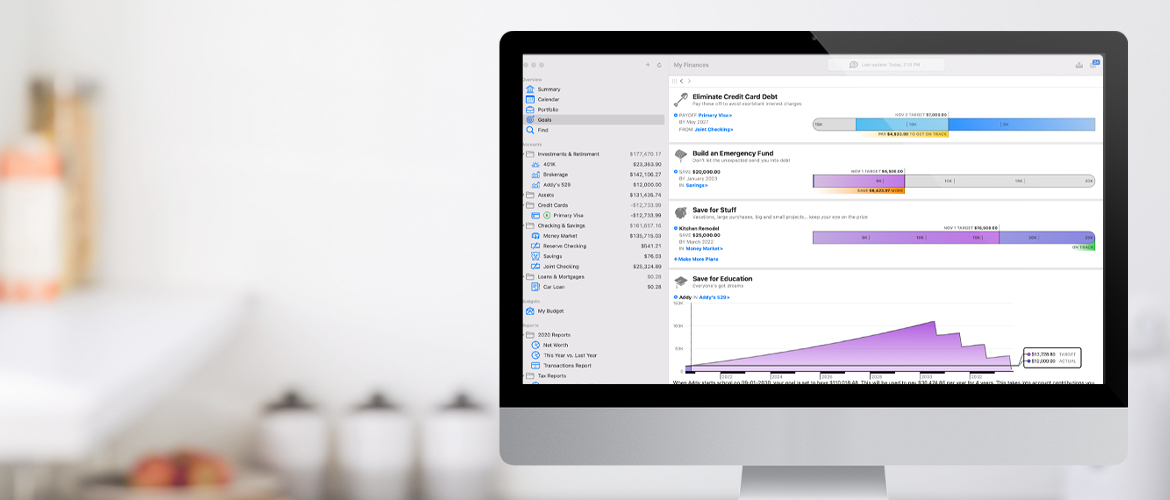

With just a few clicks of the keyboard, Banktivity subscribers can get a complete view of their entire financial picture on screen. They can see what’s coming in and what’s going out and where. If you use no other feature, that alone is worth the cost of a subscription.

But let’s talk about your budget. Rent/Mortgage payments are pretty much set. Utilities are pretty locked, but you can try to use less electricity/gas for your AC. Maybe you can bundle your mobile and internet services to get a better value and offering?

Speaking of which, during the height of Covid, I added 4 more streaming services. Of which I watch, maybe one of them twice a month now since the restrictions have been lifted. Maybe you’ve done the same? Now would be a good time to cancel a couple. Ditto music services. Maybe you put up with the commercials and go to the base Spotify membership?

Of course, you can cut back on entertainment — like the frequency of dining out or going to concerts. (I know, we get out of the pandemic, can finally go places and now I’m suggesting you cut back! Sorry.) Or maybe your grocery budget. Become a digital coupon clipper, join your local grocery stores’ loyalty programs to access special discounts. Maybe try switching from name brands to lower cost store brands. My Dad used to scour all of the grocery store fliers and “cherry pick” the lowest cost items. He’d then drive to 3 different places to get the best prices. But at an average price of $5 a gallon for gas, I’m not sure that’s a smart strategy for today.

Hope for the best (but plan for the worst)

Any money you can cut out of your discretionary budget can be reallocated to paying any outstanding debt — prioritizing those that are carrying the highest rate of interest. Which are more often than not credit cards because many carry a variable rate of interest. And by all means, resist any urge to add to that debt with any more credit card purchases.

The next area to allocate your budget savings is your emergency fund. I think I include this in every blog, and most likely will continue to do so until everyone has at least $2000 of emergency cash on hand. More is always better. And much more even better still.

As we slide closer to a recession, companies will be cutting back on hiring. And the longer this downward slide continues, their next action (if history is any indicator) will be a reduction in workforce. Job cuts and lay-offs. So now’s a good time to make sure you’re employers know how much value you bring to the workplace. A little self-promo never hurts.

You should also take advantage of any free time to add to your professional skills, expand your LinkedIn network, and update your resume. If you have a passion project or a hobby that could generate an extra stream of income, now’s the time to stop thinking about it and start doing. Like Yoda says, “Do or not do. There is no try.” And if you have items that you no longer use — clothes, bikes, appliances, sports equipment, etc. you can have a garage or tag sale. Or better still, download one of the many apps out there to help you connect your stuff to potential buyers. But if you want an app that can really improve your overall financial situation…

Download Banktivity & Try It Free for 30 Days!

As I mentioned previously, Banktivity gives you the most complete view of your financial picture and all your goals.

Designed exclusively for Mac OS and iOS, Banktivity’s suite of personal financial software helps you confidently take on all your important goals. Whether it’s paying off debt, building an emergency fund, saving for a down payment on a home, a college fund, a new car or even retirement, Banktivity’s interactive and intuitive planning tools show you where you are, what you need to do, and even projects when you’ll reach your goals.

And with the simplified Envelope Budgeting, you’ll always know what’s coming in, what’s going out and where. You can easily tweak to reallocate/reprioritize the “must haves” vs. the “nice-to-haves.” Especially helpful in uncertain times when financial trade-offs may be called for.

It all comes down to Banktivity’s commitment to helping you make the most of the money you have and ensuring you always get your money’s worth. Download it today and see what it can do for you!